A ‘New Normal’: easy come, easy go

The Covid pandemic caused a number of trend breaks, making extrapolation of historical trends practically impossible. There were many losers (retail, aviation and hospitality) but also a few Covid winners (e-commerce, medical diagnostics, streaming services and home improvement). Severely disrupted supply chains led to significantly higher logistics costs. The hitherto widely used 'just-in-time' mode was replaced by a 'just-in-case' strategy in which new supply chains were set up and larger stocks were (re)introduced into the business community.

In addition to complexity, this also led to higher costs. Increasing trade protectionism and fear of strategic dependence added additional (and also more expensive) fuel to the fire. The increased costs led to inflation, which was ultimately passed on to the end customer. In addition, governments distributed subsidies to consumers and provided subsidies and loans to affected industries. All this to keep the economy going. This artificially increased consumer spending and saved many companies from bankruptcy. However, the price of these support measures was higher government debt and even greater inflation.

A third and at least equally important contribution to inflation came from the central banks. These turned on the money tap completely; funding became almost free and was available in abundance. Not all companies responded in the same way. Some really needed the support to survive, others borrowed money at historically low rates to finance acquisitions and still others refinanced their existing debt at significantly lower rates.

“The impact of these more than significant interest rate increases is now being felt by both consumers and companies, but probably not yet to its full extent.”

Back to before, with painful consequences

Now that the pandemic seems to be in the distant past, the consequences of the measures taken are slowly becoming painfully clear.

To tame skyrocketing inflation, central banks have raised interest rates at a pace rarely seen before since early 2022. The impact of these more than significant interest rate increases is now being felt by both consumers and companies, but probably not yet to its full extent. After all, many financings have a term longer than one year, so many debt refinancings at now much higher interest rates still have to be done. It seems inevitable that this will lead to higher (interest) costs for consumers and companies.

On the consumer side, spending is now visibly declining in many sectors. The grants and handouts have largely been spent; the artificially high expenses come to an end, the wallets become empty. And the high inflation of recent years has eroded purchasing power, further affecting spending patterns. Consumers are becoming more selective in their spending.

In the aftermath of the pandemic, many companies are left with high inventories: these were often purchased at high costs and have to be financed with increasingly expensive money. Due to declining demand, the reduction of inventories also takes longer, which puts pressure on profit margins for a longer period of time. For example, we increasingly read in press releases that companies are suffering from inventory reduction among their customers; 'de-stocking' is frequently cited as a cause of disappointing sales development. It is still unclear to what extent this is indeed the reason for weak sales development, or whether there is (also) disappointing end demand among consumers.

Operating margins are also affected by increased cost prices (including wage increases!) that cannot often be passed on. Add to that higher financial costs and it is clear why earnings are under pressure. 'Pricing power' is often cited by companies, but in times of sharply rising costs it only becomes clear who can pass this on to the end customer and which companies, on the other hand, must accept lower profitability. In recent quarters we have seen that many companies report a lower margin as a result of increased input prices: apparently that pricing power is not equally strong everywhere.

The results for 2023 and the first forecasts for 2024 that companies are releasing around this time indicate that the enthusiasm was not always justified and that there is still some pain to be processed.

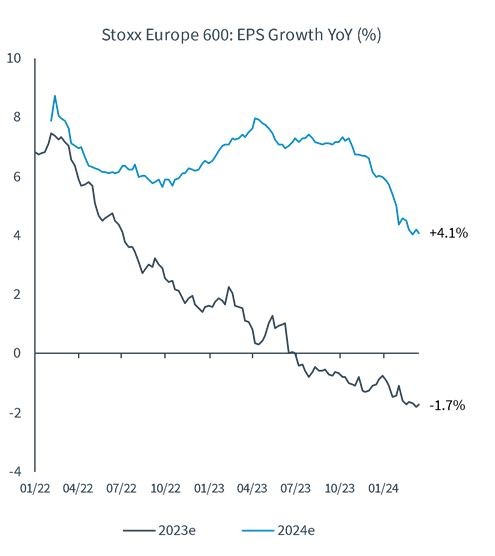

The graph below* shows the consensus expectations regarding the profits of the European Stoxx 600 index, for the years 2023 and 2024.

While analysts previously expected earnings growth for 2023, expectations were gradually adjusted: the latest figures assume a profit decline for 2023.

Growth expectations for 2024 have also already been halved; it would not be very surprising if these were adjusted further downwards in the near future.

“During the time when in many sectors, the trees were growing up into the heavens, these companies were not interesting enough for many investors.”

And now back to basics: being selective pays off again

Some companies kept a cool head during the pandemic and the recipe for their success formula unchanged. Here there was a longer-term horizon instead of a short-term maximization of turnover and/or profit. Being willing to 'leave something on the table' during euphoric times if that better suits the long-term strategy is not something every management team is willing to do.

This starts with the method of financing. Taking on debt at low interest rates is tempting, but remember that debts must be repaid and/or refinanced in due course! Long-term thinkers are often averse to debt, a phenomenon that we often see in family businesses, for example. Low or even negative interest rates are not a tailwind for debt-free companies, on the contrary. Now that interest rates are normalizing again, their strong balance sheet is again a distinctive weapon: they can continue to invest in expansion and, where necessary, in acquisitions. Due to the decreased asset prices, these acquisitions often take place at lower valuations than a few years ago.

A strong balance sheet is a good starting point, it buys you time, so to speak, but it says nothing about future turnover or profit development. In recent months, more and more turnover and profits appeared to be driven by artificial demand. The so-called earnings miss in the fourth quarter of 2023 was no less than 51%*, in other words, half of the companies performed below analysts' expectations. The reasons for the disappointments are numerous. In addition to the aforementioned reduction of inventories, a weak Chinese market, a cautious consumer and even deflation are among the causes of disappointing developments. Few companies dare to present a positive outlook for the coming periods. And most companies that do so assume a weak first half of the year, followed by a strong recovery in the second half. What that recovery is based on often remains unclear.

As always, there are companies that are growing steadily. These are usually companies that have built up a strong position over a longer period of time in markets that are less dependent on macroeconomic conditions. Healthcare, IT (particularly software but increasingly also hardware) and basic consumer goods are sectors in which many of these 'safe havens' can be found. During the time when in many sectors, the trees were growing up into the heavens, these companies were not interesting enough for many investors. Gradually, their long-term merits are resurfacing and sentiment among investors is turning.

As Warren Buffet put it, only when the tide goes out does it become clear who was swimming naked. Considering the results of companies in the European indices, it certainly seems that the boom times are behind us and the (European) water level continues to decline at a rapid pace. In that case, a safe haven, or swimming trunks, is not an unnecessary luxury.

*) Source: Kepler Chevreux

By: Lotte Timmermans | Rob Deneke | Juno Investment Partners ©

March 2024

Beware: This is a marketing communication. The information about financial markets or specific financial instruments in this document is solely intended to provide you with information about the Juno portfolio management team's view on the financial markets. This information is not an investment recommendation, nor an offer or invitation to buy or sell a financial instrument. The decision to participate in this investment fund should be taken solely on the basis of the prospectus and the key information document. You can consult these documents under 'Fund Documents' on the Fund's web page.

There are risks associated with this investment. The value of your investment may fluctuate, and past performance is no guarantee of future performance. The fund invests in stocks and stocks have a higher risk profile than bonds. The fund invests in a limited number of companies, which may lead to stronger fluctuations in the fund’s net asset value than would have been the case if the fund were less concentrated. For an overview of the risks of this fund, we refer to the risk section included in the prospectus.

Juno obtains its information from sources deemed reliable, such as annual reports and other official publications, and has taken every care to ensure that the information on which it bases its view is not incorrect or misleading. The net returns presented in this communication are based on the development of the intrinsic value of the participations.

Get in touch

Our clients are always more than welcome to drop in. There is no need for an appointment. Are you considering investing with us and want to know more about what we have to offer? We would love to bring you up to speed.